Governments’ role in the global semiconductor value chain #2

Policy Brief

Recommendation for the EU Chips Act: a long-term government value chain mapping

| This paper explains why governments need to invest in their own capacity to understand the characteristics and dynamics of the semiconductor value chain ...

Table of Contents

1. Introduction

2. Why governments need to map the semiconductor value chain

3. How to map the global semiconductor value chain

3.1 What to map?

3.2 How to map it?

4. How government value chain mapping could be institutionalized

5. Conclusion

6. SNV’s previous publications on the semiconductor value chain

7. References

Executive Summary

Since 2020, the semiconductor value chain is in the spotlight of discussions centered around security of supply, technological competitiveness, and strategic dependencies. Faced with growing geopolitical tensions and severe disruptions, governments all over the world scramble to have more control over this vital value chain. To better understand the complex semiconductor value chain and assess the competitiveness of their domestic ecosystems, governments have taken a number of measures such as hearings, round table discussions, and requests for information. While these efforts might be helpful in making sense of the current crisis, they are certainly not suitable for long-term policy planning.

This paper explains why governments need to invest in their own capacity to understand the characteristics and dynamics of the semiconductor value chain, to identify interdependencies and chokepoints. What we suggest is a long-term mapping that equips governments with the analytical base to strengthen domestic semiconductor ecosystems, deploy policy tools to curb technology transfer and establish partnerships with like-minded countries. Such a mapping would need a dedicated unit within the government to continuously assess the global semiconductor value chain. To better understand what to map and how to map it, we introduce three categories – markets, barriers to entry and technological characteristics – that need to be assessed on three different levels: inputs, production steps and end products.

This is the second paper in our series that analyzes governments’ role in the global semiconductor value chain. In our first paper, we provide an overview of the key shortcomings of a governmental supply chain monitoring as it is proposed in the EU Chips Act and argue that governments should instead work with and push industry to own the issue of supply chain monitoring.

1. Introduction

Since 2020, many governments have started efforts to better understand and assess the global semiconductor value chain. The reasons for this are threefold. First, the intensifying US–China technology rivalry has led the US government to control technology transfer to China more strictly by expanding export restrictions and investment screening efforts. The same goes for Europe, which is increasingly perceiving China as an “economic competitor” and a “systemic rival”.[1] Second, the severe disruptions to countless global supply chains induced by COVID-19-related issues have caused governments to question their dependence on foreign technology providers in general. Therefore, the US government started its “100-day supply chain review”[2] in 2021. Concurrently, as part of its new industrial strategy, the European Commission (EC) started assessing Europe’s “strategic dependencies” and “strategic capacities” in several emerging technology value chains, including semiconductors.[3] Third, the global chip shortages[4] put into question the resilience of this value chain and created further incentives for many governments to strengthen the competitiveness of their domestic semiconductor ecosystems.

In Europe and the US, the semiconductor ecosystem has not gained this level of attention from policymakers in almost a decade, if not more.[5] Policymakers’ renewed interest in this foundational technology has led to many requests for information,[6] hearings,[7] roundtable discussions, and government reports[8] trying to explain and assess this global value chain. While these are reasonable starting points for understanding this value chain, they are neither sustainable nor effective in informing long-term policy planning.

If Europe wants to manage interdependencies “in the best possible way”[9] to strengthen its “Open Strategic Autonomy” – Europe’s new compass for trade policy – one-time assessments and lengthy reports are not going to suffice. Instead, governments need to invest in their own in-depth understanding of the characteristics and dynamics of the semiconductor value chain. Government value chain mapping operationalizes “Open Strategic Autonomy” by identifying long-term interdependencies and choke points through a structured framework. Such a mapping functions as the analytical foundation to deploy policy tools to curb technology transfer, establish partnerships with like-minded countries, and strengthen domestic semiconductor ecosystems.

In the first paper of this series, we explained, with reference to the EU Chips Act proposal,[10] why the EC’s plans to intricately monitor the semiconductor value chain to anticipate and alleviate short-term supply disruptions are ill-advised. In this second paper, we argue that governments should institutionalize long-term value chain mapping as an analytical base to better inform government units working on policy tools, such as export restrictions, investment screenings, or sanctions, and to identify potential technology partnerships with allies to strengthen the resilience of this crucial value chain.

The following sections will first elaborate on why governments need to map the semiconductor value chain to inform long-term policy planning. Building on this, we provide the framework on how to map the global semiconductor value chain. Lastly, we look at how to institutionalize such government mapping within Europe. While we focus our analysis on Europe, we believe that such long-term value chain mapping would be beneficial for other regions as well.

2. Why governments need to map the semiconductor value chain

For better or worse, many governments are increasingly deploying geoeconomic measures,[11] such as export restrictions and investment screening, “to promote and defend national interests, and to produce beneficial geopolitical results.”[12]Furthermore, some technologies are deeply intertwined with national interests. This is especially true for emerging and foundational technologies (EFT), such as artificial intelligence (AI), semiconductors, and biotechnology.[13] Importantly, governments deploy these geoeconomic measures in highly complex, intertwined, and transnational value chains run almost exclusively by companies, not governments.[14] In the case of semiconductors, governments and the military together account for around 1% of global semiconductor sales and are also not producers of chips.

As understanding the global semiconductor value chain from the outside is not a trivial task, governments need to invest in their own capacity to map this critical value chain. Long-term mapping of the semiconductor value chain can provide the analytical basis for tackling different policy challenges at the intersection of the semiconductor value chain and geopolitics, such as assessing the effectiveness of geoeconomic measures, understanding potential second- and third-order effects,[15] and developing strategic international partnerships. To enhance the ministerial units working on these policy challenges, value chain mapping would need to encompass the production steps, the respective inputs (supplier markets), and end-products. For each of these, both the technology itself and the economic aspects, such as market concentration and barriers to entry, would need to be assessed.

Governments’ goals should be to establish a deep and holistic understanding of interdependencies, chokepoints, and market dynamics within the global semiconductor ecosystem, which would be beneficial when applying geoeconomic measures. Even if a government was opposed to the idea of expanding export restrictions or investment screening, it still needs to understand its own industry’s dependence on foreign technology providers to assess the potential direct and indirect impacts of foreign governments’ geoeconomic measures.

Additionally, understanding and identifying interdependencies within the value chain can also inform policymakers as to where to initiate or expand international partnerships. As the semiconductor value chain will continue to depend on the transnational division of labor, value chain mapping would allow the EC and member states to “choose when, in which area, and if, to act with like-minded partners.”[16] Connecting these insights to other policies, such as the Indo-Pacific strategy or the EU–US Trade and Technology Council (TTC),[17] would help to develop a common strategic vision of how to make the value chain more resilient in the long term and to build the united capacity to act accordingly to strengthen regional ecosystems.

To meaningfully inform these different policy tools and government activities, such continuous long-term value chain mapping requires substantial resources and dedicated units operating under a clear structure and objective within the government.[18]

3. How to map the global semiconductor value chain

The global semiconductor value chain consists of a complex network of producers, suppliers, customers, and end-customer industries. Therefore, understanding what to map and how to map it is key to creating insights into interdependencies and chokepoints for policymaking. In the following section, we propose three levels requiring mapping and introduce guiding questions that need to be addressed when analyzing each level.

3.1 What to map?

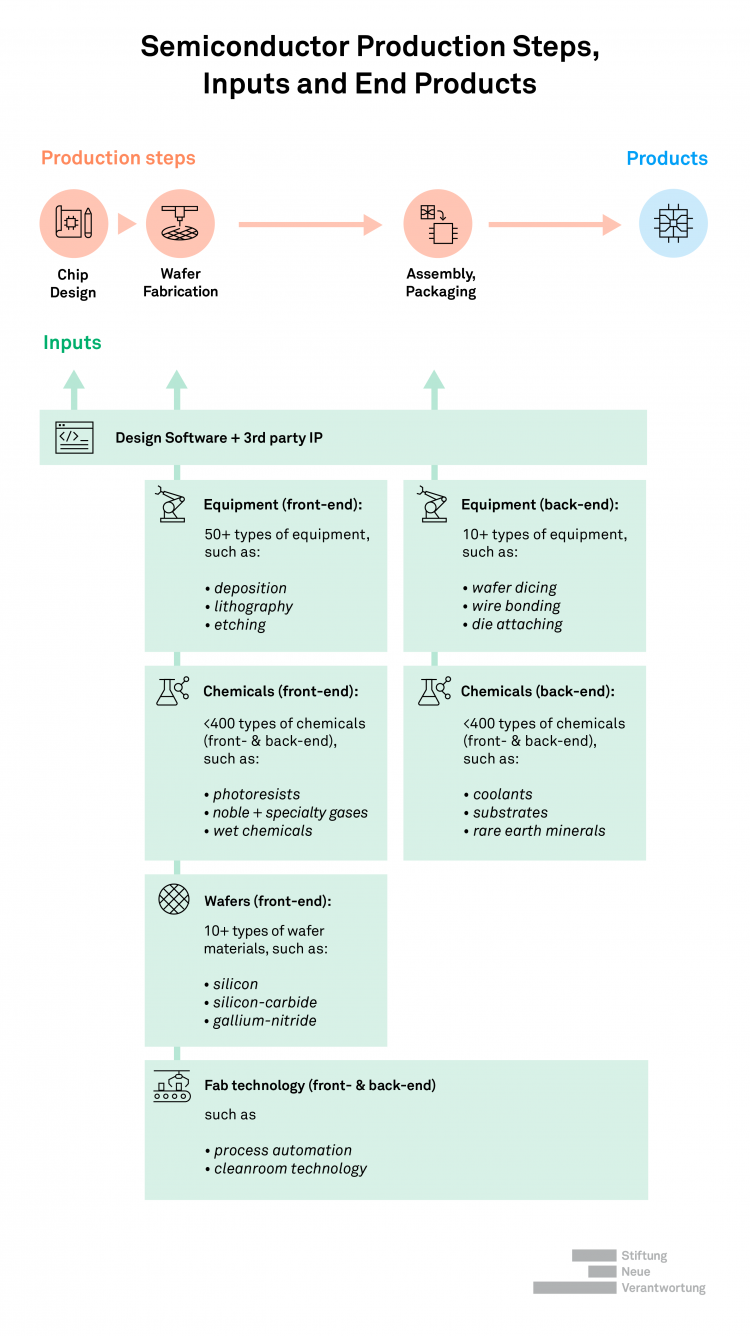

Debates on how to strengthen the resilience of the semiconductor value chain are often focused on the three production steps: 1) design, 2) front-end manufacturing, and 3) back-end manufacturing. However, this is only one puzzle piece in the semiconductor ecosystem. Government mapping of the semiconductor value chain should go further by assessing the value chain on three different levels.

Inputs

Inputs consist of the supplier markets for each production step, such as electronic design automation (EDA) tools, chemicals, equipment, wafers, process automation, and cleanroom technology. As an example, there are around 50 different types of manufacturing equipment and up to 400 different chemicals from upstream supplier markets that have very different characteristics and dynamics.[19]

Production Steps

Production steps start from chip design and evolve into front-end and back-end manufacturing. Semiconductor manufacturing is highly diverse, as it involves a huge variety of different process technologies. Designing and manufacturing a power semiconductor on silicon carbide is substantially different from that for a memory chip. Additionally, these steps are done by companies with varying business models from integrated device manufacturers (IDMs) to (fabless) chip design companies, foundries, and outsourced semiconductor assembly and test (OSAT) companies.

Products (types of semiconductors):

There are seven broad categories of semiconductors. The first four – memory, logic, micro, and analog – are integrated circuits (ICs) that make up 80% of all semiconductor sales. The other three – optoelectronics, discrete, and sensors – are sold in lower volumes under different market conditions. Many of those chips are standardized off-the-shelf products or even commodities, such as memory chips, while others are highly customized.

Thus, there is not one semiconductor value chain but countless different value chains depending on the technology and function of the final product. Even though they all significantly overlap in the majority of production steps, there are also important distinctions. For example, the characteristics, dynamics, and business models of the memory chip (DRAM and NAND) market are very different from the 5G radio frequency (RF) semiconductor market. While memory chips are based on silicon wafers and are traded as a commodity depending on economies of scale, 5G RF chips are highly specialized products reliant on complex domain expertise and different materials, such as gallium nitride.

3.2 How to map it?

Regardless of whether governments want to map a specific input (such as photoresists), a production step such as 28nm front-end manufacturing, or the market of a specific semiconductor product like memory chips, they need to ask themselves similar questions that can be structured into three broad categories: understanding the market, understanding the barriers to entry, and understanding the technology characteristics. To identify the interdependencies and chokepoints, these categories cannot be assessed in isolation, as they are deeply intertwined and complementary.

Due to the complexity and high level of division of labor in the semiconductor value chain, answering every question for every relevant market within the three levels (input, production step, and product) can only be a long-term goal requiring substantial resources. However, as a start, governments can prioritize specific markets that would be highly relevant to policy actions in the near future. By focusing on, for example, one type of input, such as EUV photoresists, the high granularity would limit the scope of information they need to collect and analyze to answer the questions below. This tailoring can function as a first step toward a better understanding of the ecosystem. From then on, they can widen their scope over time. The following are key questions for government value chain mapping:

Understanding the market for [Input, Production Step, Product]

- What is the level of market concentration in terms of companies and geographies (limited sources and single points of failure)?

- Who are the key players, and what is their business model?

- What is the market volume and growth rate?

- What is the relationship between actors up and downstream? (i.e., lock-ins)

- What are the market characteristics (i.e., off-the-shelf, high volume, highly customized, limited customers)?

Understanding barriers to entry to [Input, Production Step, Product]

- Are there economic barriers to entry (i.e. high capital intensity, economies of scale, and high labor intensity)?

- Are there technological barriers to entry (i.e. high skill/knowledge intensity and domain expertise)?

- Are there severe vendor lock-ins or path dependencies?

- What role do certification, access to IP, and licenses play?

Understanding the technological characteristics of [Input, Production Step, Product]

- What is the purpose of the technology?

- What are the technology trends (i.e., experimental stage, end of life, and serves new markets)?

- Is it relevant outside the semiconductor ecosystem (i.e., chemicals and rare earth minerals)?

- Are there national security implications? (i.e. military-utility or compromising the product)?

4. How government value chain mapping could be institutionalized

Long-term government value chain mapping would give the relevant government units a jump start to navigate strategic policy decisions. It would not be a “one-stop shop” that holds all the answers but a common starting point for the relevant policy units. Different parts of the government are already engaged in singular mapping activities in silos, often on an ad hoc basis. Economic and foreign policy departments in the member states, DGs, the newly established EU Observatory of Critical Technologies, and departments within the EU Joint Research Center are all engaged in such activities. While some of these units already collaborate across member states and share their views, such as in investment screening, there is a need for a more structured and centralized approach.

The mapping activities we are proposing would require significantly more resources, technical as well as market expertise, and access to commercial databases. Strategic long-term mapping with added value for different political actors either needs one institution that acts as a central hub or regular meetings involving all relevant stakeholders for mapping activities in the different units to ensure strong cooperation and close integration with the different entities. A standardized framework on what such mapping efforts should entail would be key to analyzing, structuring, and spreading knowledge of the semiconductor ecosystem. Additionally, the provision of structured and standardized information to the units at the national and European levels and the EC would allow for reporting and exchanging activities grounded on the same knowledge base between these actors.

Establishing long-term mapping to be overseen by one dedicated unit would ultimately reduce individual efforts from different units in conducting, evaluating, and regularly updating knowledge on the value chain. Many commercial data sets created by market analysts with decades of experience already provide valuable insights into the semiconductor industry. The envisioned mapping efforts can use these data sets as a starting point and do not need to reinvent the wheel. Once insights have been generated through mapping, regular updates on a half-year basis would be sufficient, as significant changes in market positions or chokepoints would not occur within a shorter timeframe.

5. Conclusion

Keeping track of emerging technologies and their ecosystems is a highly demanding task, but it is a prerequisite for being able to successfully utilize policy tools and strengthen international cooperation among like-minded allies. Therefore, we argue that governments need to invest in the long-term strategic mapping of interdependencies within technology ecosystems.

In line with the concept of “Open Strategic Autonomy”, value chain mapping equips governments with crucial information about interdependencies, chokepoints, and competitive positions by assessing the markets, barriers to entry, and technologies on the input, production, and product levels. In doing so, mapping informs governments on how to best deploy policy tools (such as export controls or subsidies), better anticipate second- and third-order effects, and strengthen international cooperation.

As we are discussing a highly complex transnational value chain with a high level of division of labor, exhaustive mapping cannot be realized in the short term. However, the introduced framework can also be used to look at a specific supplier market, production step, or semiconductor type. As units working on planned export or investment restrictions or other economic measures often focus only on a small section of the semiconductor value chain, the questions can be used as guidance. Most importantly, the success of such mapping depends on governments’ willingness to invest in their own capacity to assess and understand complex technology ecosystems. If the US and European governments are willing to spend dozens of billions of Euros in subsidies for semiconductor companies, they should at least invest dozens of millions of Euros (1000 times less) in their own capacity to analyze the semiconductor value chain.[20]

This is the second paper in our series on the roles governments play in the global semiconductor value chain. With reference to the EU Chips Act, the first paper explained the shortcomings of the proposed monitoring mechanism in Pillar 3 and argued that the short-term anticipation of disruptions and crises is a responsibility of the industry. Based on this, we differentiated between industry supply chain monitoring and government value chain mapping, which was introduced in this paper. Government mapping can address areas where policymakers can make a difference in a sustained manner; specifically, governments can improve long-term value chain resilience by deploying strategic policy tools and strengthening international partnerships.

SNV’s previous publications on the semiconductor value chain

- Governments’ role in the global semiconductor value chain #1 – Analysis of the EU Chips Act: Challenges of government monitoring of the supply chain

-

Jan-Peter Kleinhans, Julia Hess and Wiebke Denkena, June 2022

We analyze the shortcomings of the European Commission’s proposed semiconductor supply chain monitoring. We argue that a highly granular supply chain monitoring to foresee and alleviate short-term disruptions and shortages cannot be meaningfully done by governments.

- China’s rise in semiconductors and Europe: Recommendations for policy makers

-

Jan-Peter Kleinhans and John Lee, December 2021

We assess Europe’s dependency on Chinese companies at certain stages of the value chain from the national security, technological competitiveness, and supply chain resilience perspectives. We argue that the EU’s future semiconductor strategy should include three focus areas: chip design, back-end manufacturing, and supply chain resilience through constant mapping of interdependencies. This is a joint publication with the Mercator Institute for China Studies (MERICS).

- Understanding the global chip shortages: Why and how the semiconductor value chain was disrupted

-

Jan-Peter Kleinhans and Julia Hess, November 2021

In this paper, we explain exactly what disrupted the global chip value chain and why it is not a single shortage but multiple shortages happening concurrently at different steps for different reasons.

- Mapping China’s semiconductor ecosystem in global context: Strategic dimensions and conclusions

-

John Lee, Mercator Institute for China Studies (MERICS), and Jan-Peter Kleinhans, June 2021

Our report analyzes the competitiveness of China’s chips industry across all production steps and supplier markets. We draw conclusions across three strategic dimensions: industry competitiveness, national security, and resilience. This is a joint publication with the Mercator Institute for China Studies (MERICS).

- Who is developing the chips of the future?

-

Jan-Peter Kleinhans, Pegah Maham, Julia Hess, and Anna Semenova, June 2021

Our third paper dives into the national “R&D power” to better understand who is developing the chips of the future through a quantitative analysis of three of the leading global semiconductor conferences since 1995 (IEDM, ISSCC, and VLSI).

- The lack of semiconductor manufacturing in Europe: Why the 2nm fab is a bad investment

-

Jan-Peter Kleinhans, April 2021

Our second paper explains why there is little business case for a 2nm fab in Europe, which, in turn, means that there is a real risk of wasting billions of Euros in public and private money.

- The Global Semiconductor Value Chain: A Technology Primer for Policy Makers

-

Jan-Peter Kleinhans and Dr. Nurzat Baisakova, October 2020

Our first publication on semiconductors provides an overview of the global semiconductor value chain, its interdependencies, market concentrations, and chokepoints. The process steps, their characteristics, and the major players are depicted to understand why this value chain is highly innovative and transnational but at the same time very fragile and thus, not resilient.

This content is subject to a Creative Commons license (CC BY-SA 4.0). The reproduction, distribution and publication, modification or translation of the content of the Stiftung Neue Verantwortung marked with the “CC BY-SA 4.0” license as well as the creation of products derived from it, are permitted under the terms “Attribution” and “ShareAlike”. Detailed information on the license conditions can be found at Creative Commons.

7. References

[1] European Commission. 2019. “EU-China – A strategic outlook.” JOIN(2019) 5 final.

[2] The White House. 2021. “Building Resilient Supply Chains, Revitalizing American Manufacturing, And Fostering Broad-Based Growth.”

[3] European Commission. 2021. “Strategic dependencies and capacities.” SWD(2021) 352 final.

[4] Jan-Peter Kleinhans and Julia Hess. 2021. “Understanding the global chip shortages: Why and how the semiconductor value chain was disrupted.” Stiftung Neue Verantwortung.

[5] Electronic Leaders Group. 2014. “A European Industrial Strategic Roadmap for Micro- and Nano-Electronic Components and Systems.”

[6] European Commission. 2022. “European Chips Survey: Stakeholder Survey on European Chip Demand.”; Bureau of Industry and Security. 2021. “Risks in the Semiconductor Manufacturing and Advanced Packaging Supply Chain.” BIS-2021-0011; Bureau of Industry and Security. 2021. “Notice of Request for Public Comments on Risks in the Semiconductor Supply Chain.” BIS-2021-0036; U.S. Department of Commerce. 2022. “Incentives, Infrastructure, and Research and Development Needs To Support a Strong Domestic Semiconductor Industry.” DOC-2021-0010-0001.

[7] U.S.-China Economic And Security Review Commission. 2022. „U.S.-China Competition in Global Supply Chains.“ Hearing 9 June 2022.

[8] European Commission. 2022. “A Chips Act for Europe.” SWD(2022) 147 final; The White House. 2021. “Building Resilient Supply Chains, Revitalizing American Manufacturing, And Fostering Broad-Based Growth.”

[9] European Commission. 2022. “Trade Policy Review: Open Strategic Autonomy.”

[10] In February 2022, the EC proposed the European Chips Act, which is accompanied by four documents (Communication, Regulation, and Recommendation). In May 2022, the Staff Working Document (SWD) was published. The EU Chips Act is divided into three sections: (1) “Chips for Europe Initiative” with the goal of supporting investment into cross-border and openly research, development and innovation infrastructures; (2) mid-term security of supply actions to enhance semiconductor production capacity in Europe; and (3) a monitoring mechanism and instruments for crisis response.

[11] Anthea Roberts, Henrique Choer Moraes and Victor Ferguson. 2018. “The Geoeconomic World Order.” Lawfare Blog.

[12] Robert D. Blackwill and Jennifer M. Harris. 2017. “War by Other Means.” Harvard University Press.

[13] Jeffrey Ding and Allan Dafoe. 2020. “The Logic of Strategic Assets: From Oil to Artificial Intelligence.”

[14] Henry Farrell and Abraham L. Newman. 2019. „Weaponized Interdependence: How Global Economic Networks Shape State Coercion.“

[15] The US export restrictions against Huawei are an example for multiple second-and third-order effects, as they indirectly contributed to the global chip shortages and strengthened the market position of Chinese chip design companies. Chinese semiconductor companies and end-customer industries (smartphone and ICT manufacturers) started stockpiling chips and supplies in fear of also being targeted by US export restrictions in the future, which in turn further amplified the global chip shortages. Another third-order effect is the rise of Chinese chip design company UNISOC. In smartphone chipsets, UNISOC had a global market share of 4% in Q4 2020 and 11% in Q1 2022, while Huawei (HiSilicon) went from 7% in Q4 2020 to 1% in Q1 2022. In the same timeframe, many HiSilicon engineers left the company to work for UNISOC.

[16] Suzana Anghel, et al. 2020. “On the path to ‘strategic autonomy.’” European Parliamentary Research Service.

[17] Having an informed exchange within the different working groups, such as the EU-US TTC Working Group 3 (WG 3), on “Secure Supply Chains” can have a long-term impact through aligned common actions to protect the EU and US interests and values rather than focusing only on short-term disruptions.

[18] John VerWey. 2022. “Testimony before the U.S.-China Economic and Security Review Commission.” 9 June 2022 Hearing on “U.S.-China Competition in Global Supply Chains”.

[19] Antonio Varas, et al. 2021. “Strengthening the Global Semiconductor Supply Chain in an Uncertain Era.” SIA x BCG.

[20] Jan-Peter Kleinhans. 2022. “Testimony before the U.S.-China Economic and Security Review Commission.” 9 June 2022 Hearing on “U.S.-China Competition in Global Supply Chains”.

Julia Hess, Jan-Peter Kleinhans